I’ve been a trader and investor for 44 years. I left Wall Street long ago—-once I understood that their obsolete advice is designed to profit them, not you.

Today, my firm manages around $5 billion in ETFs, and I don’t answer to anybody. I tell the truth because trying to fool investors doesn’t help them, or me.

In Daily H.E.A.T. , I show you how to Hedge against disaster, find your Edge, exploit Asymmetric opportunities, and ride major Themes before Wall Street catches on.

Table of Contents

H.E.A.T.

-11% SOX pullback from June high | $11B Semi ETF outflows, late June | BBB- Oracle's new rating — one notch above junk | +13pts IGV vs. SOX, trailing 3 weeks |

The first warning sign wasn't a bad number. It was a good number that stopped working.

Micron shares ripped 15.7% after its June 25 earnings print. Samsung followed days later with record quarterly profit. Memory prices kept rising. And the semiconductor tape cracked anyway — the Philadelphia Semiconductor Index has fallen more than 11% from its June high, with roughly $11 billion pulled from semiconductor ETFs in late June alone.

That is the tell.

The market isn't asking whether AI infrastructure demand exists anymore. It obviously does. It's asking whether the next dollar of capital spending earns an acceptable return — and whether the stocks already priced in more perfection than the business can deliver. Micron's rally never re-anchored the group. Within days, Samsung's record quarter failed to calm the tape, the chip index rolled over, and the market started treating memory strength as evidence the cycle had peaked, not as fresh fuel to run higher.

PART I: THE GOOD-NEWS TEST

Since Micron's print, the semiconductor complex has led the tape lower almost across the board. Semiconductor-capital-equipment makers have been hit hardest, as the market starts pricing whether the next leg of AI capex actually clears a return hurdle. Optical names — the market's favorite proxy for "AI is unstoppable" — have reversed sharply, giving back a large share of their year-to-date gains in a matter of weeks.

The damage runs wide. A broad basket of AI-infrastructure-adjacent names — chip designers, cloud-buildout financers, memory suppliers, and packaging and test names — is down double digits together, with high correlation across the group. Even the analog chipmakers, whose demand is more auto- and industrial-driven than AI-driven, have been caught in the downdraft. Korean memory stocks have followed suit, with the broader Korean index entering correction territory alongside sharp single-day drawdowns in the country's two largest memory producers.

“Good numbers stopped being enough the moment the market started pricing perfection instead of growth.” |

None of this means the memory shortage is over. TrendForce's latest data shows Q3 conventional DRAM contract prices still rising 13 to 18% quarter-over-quarter, and NAND up 10 to 15% — both decelerating hard from roughly 58 to 62% and 55 to 60% gains, respectively, in the second quarter. Memory isn't collapsing. The rate of price acceleration is slowing, and the market is starting to price the next derivative: supply response, demand elasticity, and capex discipline. The easy multiple expansion in memory stocks may already have been made, even if the pricing cycle itself hasn't fully run its course.

PART II: THE CREDIT TAPE MOVES FIRST

The equity market can debate for months whether AI software monetizes. The bond market is already asking whether the capex machine can be financed. Oracle was downgraded to one notch above junk, with the rating agency explicitly citing the scale of investment required by its AI infrastructure buildout. Amazon's own AI-linked borrowing priced at a higher cost amid signs of investor fatigue, after roughly $244 billion of hyperscaler investment-grade bond issuance so far this year. Investors are increasingly demanding higher risk premiums on longer-dated hyperscaler paper.

CREDIT WATCH This rhymes with the telecom fiber build-out of 1998 to 2001 — hundreds of billions raised to fund capacity ahead of proven demand. The balance sheets funding today's AI buildout are considerably stronger than WorldCom's or Global Crossing's were. The financing dynamic — spend now, prove the return later, let the bond market keep the receipts — is not a new story. It's an old one wearing a new label. |

This is exactly the kind of signal where credit investors move first and equity investors catch up later. Oracle's downgrade is not, on its own, proof that the AI capex cycle is broken. It is proof that the market is now underwriting these commitments with more scrutiny than it was six months ago.

PART III: THE ROTATION BENEATH THE SURFACE

Since Micron's print, the S&P is up a modest 1% — but look at what's actually working underneath that number. Healthcare and Financials are each up roughly 8%, while Materials and Technology are the only sectors in the red. Low Volatility and Yield factors are outperforming High Beta, Momentum, and Growth. That is not what a market euphoric about AI looks like. It's what a market rotating out of its most crowded trade looks like.

To be clear about what this is not: this is not “AI is over.” Global equity funds just posted their largest weekly inflow in three weeks, with technology funds leading sector inflows. Capital isn't fleeing AI — it's getting more selective about which part of the AI stack it's willing to pay up for. The leadership is narrowing and rotating, from the infrastructure being built toward the return on what's already been built.

PART IV: SOFTWARE GETS SELECTIVE, NOT UNIVERSAL

The software trade is not simply “back.” The market is separating systems of record and workflow infrastructure from point-solution software. Large incumbents with deep installed bases and distribution, vertical systems of record, AI-infrastructure and data platforms, and cybersecurity names are being revalued as the places AI must plug into in order to actually convert into labor-cost savings. Creative and point-solution tools have bounced with the group, but they remain structurally more exposed to AI-native substitution — that strength looks more like a trading bounce than a change in thesis, until proven otherwise.

The market's mistake this year was treating software as the victim of AI. In most enterprise categories, software is the distribution layer through which AI actually reaches the labor budget. A system of record doesn't disappear because a model gets smarter — it becomes more valuable, because it owns the workflow, the permissions, the data history, and the audit trail the model needs in order to act. Private AI lab valuations have exploded even as public software was broadly de-rated. That gap between private AI enthusiasm and public software skepticism was always going to close from one side or the other. Right now, it's closing from software's side.

This is not the end of the AI trade. It is the end of the market paying any price for AI capex without visible proof of return.

WINNERS & LOSERS

COMPANY / SECTOR | VERDICT | WHY IT MATTERS | RISK |

ServiceNow (NOW) | System-of-Record Winner | Owns the workflow layer AI needs to plug into; installed base and distribution buy time to reprice for an agentic world. | Valuation already reflects a good deal of the AI-optionality thesis. |

Salesforce (CRM) / HubSpot (HUBS) | Repricing Candidate | Large installed base, but the seat-based model still needs to be rebuilt around consumption and outcomes. | Slower to execute the pivot than System-of-Record peers already moving. |

Datadog (DDOG) / Snowflake (SNOW) / MongoDB (MDB) | AI Infrastructure Winner | Sits underneath the agent layer — more agents mean more usage, more inference, more data volume. | Valuations already assume durable growth reacceleration. |

Palo Alto Networks (PANW) / CrowdStrike (CRWD) / Okta (OKTA) | Durable Category | Security spend is harder to cut and harder to disrupt with a single point AI tool. | Platform consolidation risk if one vendor bundles competitively. |

Tyler Technologies (TYL) / Guidewire (GWRE) / Veeva (VEEV) / Workday (WDAY) | Vertical Moat | Deep, sticky vertical data and workflows that horizontal AI tools can't easily replicate. | Smaller total addressable market than horizontal SaaS peers. |

KLA (KLAC) / Lam Research (LRCX) | Capex-Return Pressure | Semi-cap equipment is a direct read on whether AI capex keeps accelerating. | Any confirmed capex discipline from customers hits order books directly. |

Ciena (CIEN) / Coherent (COHR) / Applied Optoelectronics (AAOI) / Fabrinet (FN) | Multiple Reset | The optical basket was priced as an AI-is-unstoppable proxy; that assumption is now being tested. | This may be a valuation reset rather than an actual demand collapse. |

ARM, MRVL, MTSI, TTMI, ORCL, CRWV, NBIS, APLD, IREN, Kioxia, WDC, CAMT, FORM, AMKR | AI-Adjacent Drawdown | Broad basket of AI-infrastructure-adjacent names down double digits together, in high correlation. | High correlation cuts both ways — a rebound in one likely lifts the whole basket. |

Adobe (ADBE) / Figma (FIG) | Watch List | Bounced with the group, but structurally more exposed to AI-native substitution of creative workflows. | Could still prove durable if AI gets embedded into their own workflow instead of ceding it. |

PRESSURE POINTS

PRESSURE POINT | WHAT TO WATCH | TIME HORIZON |

Oracle's next earnings / credit update | Further downgrade or stabilization signals whether the AI-infra credit story is contained to one name or spreading. | Q3 2026 |

Hyperscaler bond issuance & spreads | Watch pricing and demand on the next Amazon, Microsoft, Meta, or Google AI-linked bond deal. | Ongoing — event-driven |

TrendForce Q4 DRAM/NAND ASP guidance | Confirms whether pricing deceleration continues or reaccelerates. | Q4 2026 |

3Q software earnings season | Tests the “SaaS checks are healthy” claim currently driving the software rotation. | Aug–Sep 2026 |

Tech fund flow data | Confirms whether this is rotation within AI or the start of a broader outflow. | Weekly — ongoing |

CREDIBILITY FIREWALL

SOURCED/REPORTED | MODELED/INFERRED | EDITORIAL VIEW |

Oracle downgraded to BBB-, one notch above junk; the rating agency cited the scale of AI infrastructure investment. | Downgrade read as an early signal that the AI capex financing model faces real scrutiny, not an isolated credit event. | This is the single most important data point in this issue. Credit investors are front-running the equity market's AI-ROI debate. |

Micron shares rose 15.7% after its June 25 earnings; the Philadelphia Semiconductor Index fell more than 11% from its June high with ~$11B of ETF outflows in late June. | Trailing three-week IGV vs. SOX outperformance of roughly 13 points (desk calculation from index levels). | Good numbers no longer buy semis a bid. That's an expectations problem, not a fundamentals problem — yet. |

TrendForce forecasts Q3 conventional DRAM contract prices up 13–18% QoQ (vs. 58–62% in Q2); NAND up 10–15% (vs. 55–60%). | Deceleration read as the market pricing peak-shortage conditions, not a pricing reversal. | Memory isn't collapsing. The multiple on memory stocks may already have priced the best quarter they're going to get. |

Global equity funds posted their largest weekly inflow in three weeks in the week ended July 8, with tech funds leading sector inflows. | Capital is not fleeing AI broadly — it's getting selective within the AI complex. | Treat this as a rotation story, not a capitulation story. That distinction changes what you should be buying, not just what you should be selling. |

Anthropic was valued at $965 billion after its May funding round, more than double its February valuation. | The gap between exploding private AI lab valuations and de-rated public software multiples is a dislocation, not a permanent verdict. | That gap closes from one side or the other. Recent price action suggests it's starting to close from software's side. |

BEAR CASE: WHY THIS COULD BE NOISE

BEAR CASE SPOTLIGHT Quarter-end rebalancing, index-reconstitution flows, and a rise in the 10-year yield can explain a meaningful share of this rotation without any AI-specific story at all. Memory prices are still rising quarter over quarter — nothing in the TrendForce data shows an outright decline. Oracle's downgrade reflects the scale of one company's specific commitments, not a sector-wide financing freeze; other hyperscalers with stronger balance sheets haven't seen similar credit actions. And software's seat-based pricing problem hasn't been solved by three weeks of outperformance — if third-quarter checks disappoint, this bounce reverses fast. We've seen this head-fake before. |

FIVE THINGS TO DO WITH THIS INFORMATION

1. Don't read this as “AI is over.” Tech fund flows are still positive — check the flow data before assuming capitulation, not just the price action in the AI-adjacent basket.

2. Watch Oracle's credit spreads and the next hyperscaler bond deal pricing. That's the leading indicator here, not the equity tape.

3. Get selective in software. Favor systems of record, workflow infrastructure, cybersecurity, and data infrastructure over point solutions and creative tools.

4. Track TrendForce's Q4 DRAM/NAND guidance. Continued deceleration confirms the capex-discipline thesis; a reacceleration argues this was just seasonal repositioning.

5. Use 3Q software earnings season as the real referendum. The “SaaS checks are healthy” claim driving this rotation gets tested in August and September — that's what determines if this has legs into the second half.

The longest-running theft in American history?

Porter Stansberry's argument: when new money is printed, the dollars you already hold

quietly lose purchasing power, a "theft" you never see on any statement. Whether or not

you agree, the Porter & Company Porter Portfolio Index ETF (PCPP) was built for

investors who'd rather hold a diversified mix than sit in cash. It tracks a rules-based index

split roughly four ways: P&C insurers, capital-efficient equities, hard assets, and

short-term fixed income.

Investing involves risk including possible loss of principal.

Read the prospectus at porterandcofunds.com.

Consider the fund's investment objectives, risks, charges, and expenses carefully before

investing. This and other information are in the prospectus at PorterandCoFunds.com or (833)759-6110; read it carefully before investing. Investing involves risk, including possible loss of principal. PCPP is new and non-diversified. Distributed by Foreside Fund Services, LLC.

News vs. Noise: What’s Moving Markets Today

Over the weekend all the Wall Street desk notes were about the semiconductor sell off being over. Someone forgot to tell the market…..

SMH looks like a short at the 50 day moving average.

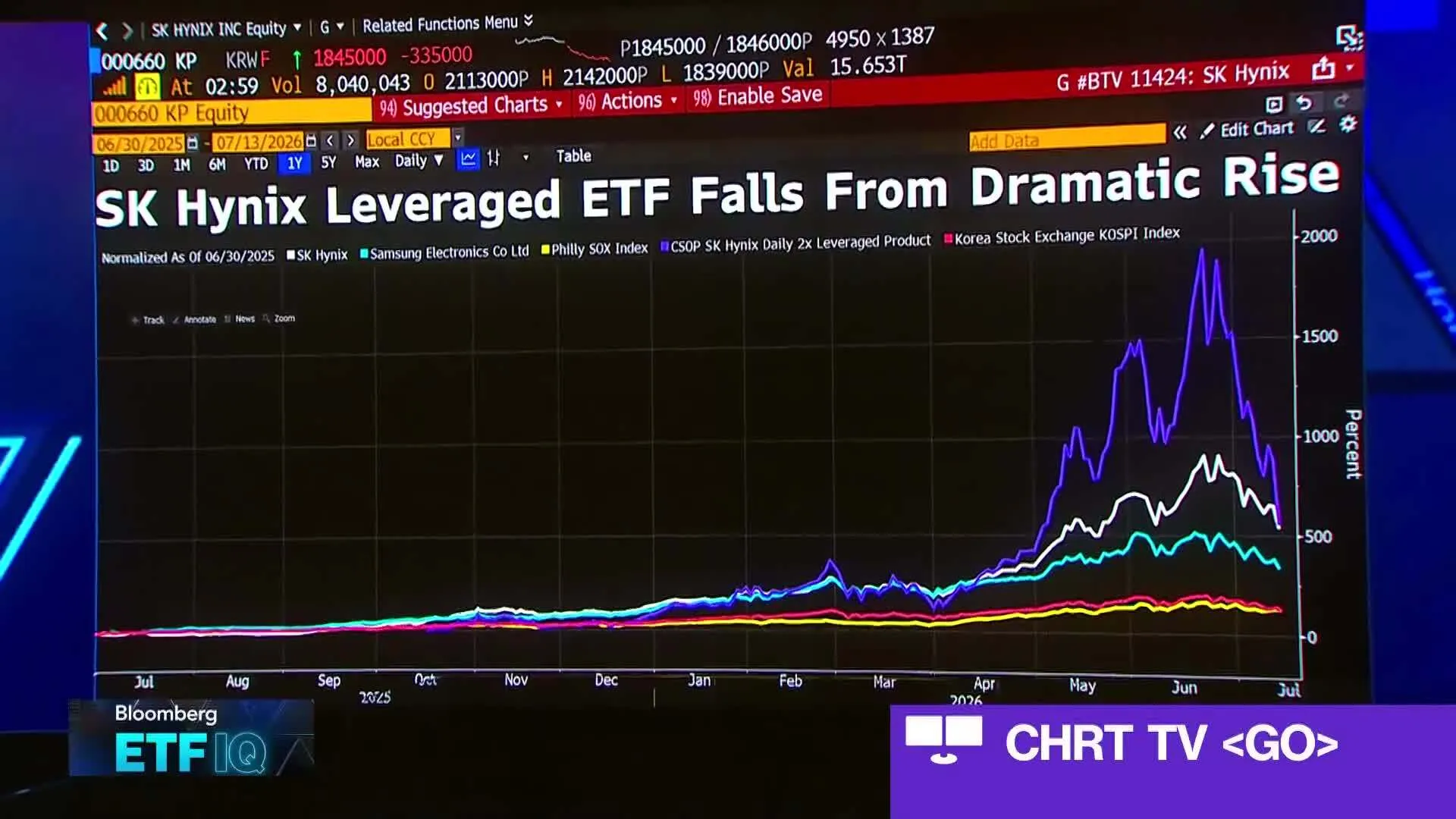

Meanwhile in Korea…..

Korea Financial Supervisory Service: As of July 13, the cumulative total of over 1.2 million leveraged retail accounts across the Korean market triggered margin calls, with approximately 320,000–360,000 accounts fully forcibly liquidated by brokers (principal wiped out, some with partial negative balances owed to brokers)

EWY also looks like a short…..

I talked about the HALO (heavy asset low obsolescence) names yesterday, and they are pretty much the only things that don’t look like shorts here.

Steel…

Natural Gas…

Energy…..

Wish there was an ETF for that :)

Today is CPI. Fed Governor Waller, who was a strong dove when he was a contender to be chair, seemingly has flipped somewhat hawkish….

If we get another hot reading on core inflation this week, then the FOMC will need to consider tightening monetary policy in the near term."

ETF News

Launched today………….

A Stock I’m Watching

Pretty much the only tech name that looks ok. Undercut and rally at the $209.84 low, I’d use that area as a stop. If this continues to unravel they will eventually get everything.

In Case You Missed It

Great conversation on wide ranging topics with Kenny Polcari…

The H.E.A.T. (Hedge, Edge, Asymmetry and Theme) Formula is designed to empower investors to spot opportunities, think independently, make smarter (often contrarian) moves, and build real wealth.

The views and opinions expressed herein are those of the Chief Executive Officer and Portfolio Manager for Tuttle Capital Management (TCM) and are subject to change without notice. The data and information provided is derived from sources deemed to be reliable but we cannot guarantee its accuracy. Investing in securities is subject to risk including the possible loss of principal. Trade notifications are for informational purposes only. TCM offers fully transparent ETFs and provides trade information for all actively managed ETFs. TCM's statements are not an endorsement of any company or a recommendation to buy, sell or hold any security. Trade notification files are not provided until full trade execution at the end of a trading day. The time stamp of the email is the time of file upload and not necessarily the exact time of the trades. TCM is not a commodity trading advisor and content provided regarding commodity interests is for informational purposes only and should not be construed as a recommendation. Investment recommendations for any securities or product may be made only after a comprehensive suitability review of the investor’s financial situation.© 2026 Tuttle Capital Management, LLC (TCM). TCM is a SEC-Registered Investment Adviser. All rights reserved.